When you get caught driving someone else's car without insurance, liability splits between you and the owner — and your violation record determines who gets hit hardest at renewal.

The owner's policy takes the first hit, but your violation record determines the lasting damage

When you're caught driving uninsured in a borrowed car, the ticket typically goes to you as the driver, but the insurance consequences split between you and the vehicle owner. If the owner had an active policy on the vehicle, their insurer may face a claim or coverage question when the violation surfaces. If the owner had no active policy, you both face uninsured driver violations — you for operating without coverage, the owner for allowing an uninsured vehicle on the road.

The violation adds points to your driving record in most states, triggering a rate increase that lasts 3-5 years on your own policy. The owner faces a different problem: their insurer may non-renew the policy at the next term or reclassify them as high-risk if the violation suggests they're lending vehicles to uninsured drivers. The rate impact depends on whether the insurer treats the incident as a coverage lapse, an excluded driver violation, or evidence of material misrepresentation on the policy application.

If you already have points on your record from prior violations, this incident compounds the problem. A second or third violation within a rolling 12-24 month window pushes many drivers over the threshold where preferred carriers decline coverage entirely, leaving standard or non-standard markets as the only options. The owner's exposure depends on their own violation history and whether their insurer views the incident as an isolated event or a pattern of risky behavior.

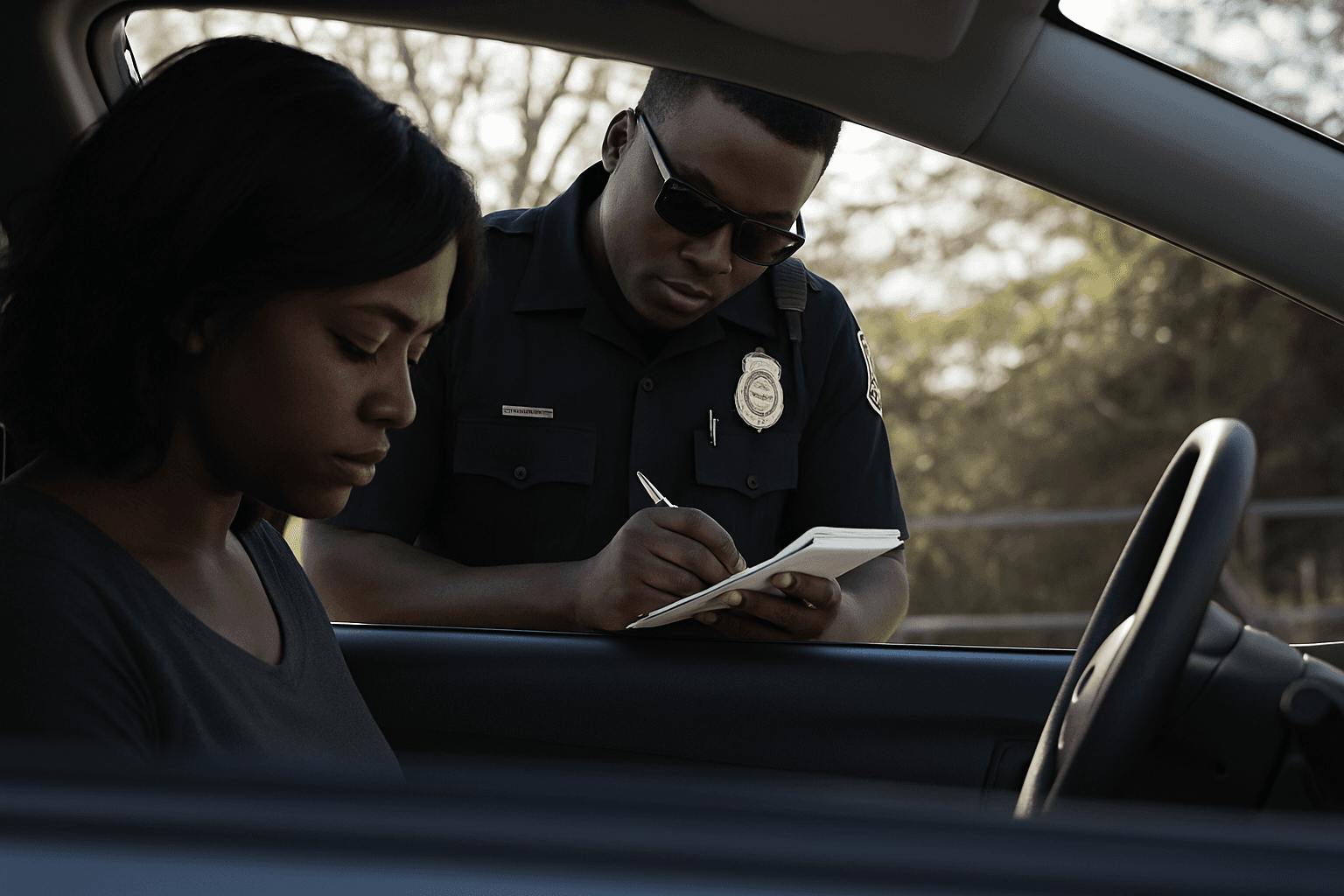

Who gets the ticket and who gets the points

The driver receives the citation for operating an uninsured vehicle. This violation adds points to your driving record — typically 2-4 points depending on the state — and stays on your record for 3-5 years. The points trigger a surcharge on your own auto insurance policy at the next renewal, even if you weren't driving your own car when cited.

The vehicle owner may receive a separate citation for allowing an uninsured vehicle to be operated, or for failing to maintain required coverage. In some states, the owner faces a vehicle registration suspension until proof of insurance is filed. In others, the owner's insurer receives notification of the violation through state DMV reporting systems, triggering a policy review or non-renewal notice.

If the owner's policy was active at the time of the stop but you weren't listed as a covered driver, the insurer may treat the incident as an excluded driver violation. This creates a coverage gap: the owner's policy won't cover any accident you caused while driving, but the violation still appears on the owner's claims history and may trigger a rate increase or policy cancellation.

Compare rates from carriers that work with drivers who have points

Standard carriers surcharge heavily after violations. These specialists price your specific record differently.

Get Your Free Quote✓ Violation Specialists✓ No Obligation✓ Licensed Carriers✓ All Point Levels

How the violation affects your insurance rates and coverage options

An uninsured driver violation triggers a surcharge on your own policy that typically raises your premium 20-40% for 3-5 years. The exact increase depends on your current violation count, the severity of the citation, and your carrier's surcharge schedule. If this is your first violation, most preferred carriers will renew your policy with the surcharge applied. If you already have points from prior tickets or accidents, the new violation may push you over the threshold where your current carrier declines to renew.

Carriers view uninsured driver violations as high-risk indicators because they suggest either financial instability or deliberate non-compliance. If your policy is non-renewed, you'll need to shop standard or non-standard markets where premiums run 40-80% higher than preferred rates. Non-standard carriers specialize in insuring drivers with violation records, but they require higher liability limits and offer fewer discount options.

The violation stays on your insurance record longer than it stays on your DMV record in most states. DMV points may expire after 3 years, but insurers typically pull 5-year driving records at renewal. You'll see the surcharge reflected in your premium for the full 5-year window unless you request a rate review after the DMV points drop off.

What happens to the vehicle owner's coverage and rates

The vehicle owner's insurer reviews the violation during the next policy renewal and assesses whether the incident represents a coverage risk. If the owner allowed you to drive without verifying that you had your own insurance, the insurer may interpret this as negligent lending behavior and apply a surcharge or non-renew the policy. If the owner told the insurer they were the only driver but the violation proves otherwise, the insurer may treat this as material misrepresentation and cancel the policy mid-term.

If the owner's policy was active and you were listed as an occasional driver, the violation affects the owner's rate indirectly. The insurer applies a surcharge based on your violation, not the owner's driving record, but the owner's premium increases because their policy now covers a higher-risk driver. The surcharge stays in place until you're removed from the policy or the violation ages beyond the carrier's lookback window.

If the owner had no active policy at the time of the stop, they face a registration suspension in most states until they file proof of insurance with the DMV. Reinstating the registration requires purchasing a new policy, paying reinstatement fees, and in some states, filing an SR-22 certificate. The new policy will be rated as high-risk, with premiums 50-100% higher than standard rates, because the coverage lapse signals non-compliance.

When SR-22 filing is required and who has to file it

SR-22 filing requirements depend on whether the violation triggered a license suspension or whether your state mandates filing for uninsured driver citations. In most states, a first-time uninsured driver violation does not require SR-22 unless the violation led to a license suspension or occurred during a period when your license was already suspended for prior violations.

If SR-22 is required, you as the driver must file it, not the vehicle owner. The filing attaches to your driver's license and stays in place for 1-3 years depending on state requirements. Your insurer files the SR-22 certificate with the state DMV and monitors your coverage continuously. If your policy lapses or is cancelled during the filing period, the insurer notifies the DMV and your license is suspended until you reinstate coverage and file a new SR-22.

The vehicle owner may face separate SR-22 requirements if the state issued a registration suspension or if the owner's license was suspended for allowing an uninsured vehicle to be operated. This creates dual filing obligations: you file SR-22 to reinstate your driver's license, the owner files SR-22 to reinstate vehicle registration. Each filing carries separate fees and insurance surcharges.

What to do immediately after the citation to limit rate damage

Purchase your own auto insurance policy within 24-48 hours of the citation if you don't already have one. Carriers view immediate coverage purchase as evidence of compliance, which may reduce the severity of underwriting decisions at renewal. If you already have a policy, contact your insurer to disclose the violation before they receive DMV notification. Voluntary disclosure sometimes triggers a smaller surcharge than discovery through automated reporting.

Request a copy of the citation and verify the violation code and points assessed. Some uninsured driver citations carry lower point values if the driver can prove they had coverage under a different policy at the time of the stop. If you were covered under a parent's or spouse's policy but didn't have proof of insurance at the stop, submit that documentation to the court and request a dismissal or reduction to a lesser violation.

If the citation pushed your total point count over your state's suspension threshold, attend a defensive driving course before the DMV processes the suspension. In some states, completing an approved course removes points from your record or delays the suspension, giving you time to adjust your insurance coverage before carriers see the suspension flag. The course must be completed before the suspension becomes active to receive credit.

How long the violation affects rates and when you can shop for better coverage

The uninsured driver violation affects your insurance rates for 3-5 years from the citation date, depending on your carrier's surcharge schedule. Most carriers apply the full surcharge for the first 3 years, then reduce it by 50% in year 4 before removing it entirely in year 5. The violation stays on your driving record during this entire window, so any carrier you shop will see it and apply their own surcharge.

You can shop for new coverage immediately after the violation, but expect limited options if you already have other violations on your record. Preferred carriers typically decline drivers with 2 or more violations in a rolling 3-year window, leaving standard and non-standard markets as your primary options. Standard carriers offer moderate surcharges but require higher liability limits. Non-standard carriers accept higher-risk drivers but charge premiums 40-80% above preferred rates.

The best time to shop is 30-60 days before your current policy renewal, after you've completed any court-ordered defensive driving courses or SR-22 filing requirements. This gives new carriers a complete picture of your violation status and allows them to quote accurate rates. Request quotes from at least 3 carriers in each tier — preferred, standard, and non-standard — to identify the lowest available rate for your violation profile.